Patents and R&D projects, such as the development of new pharmaceuticals, are subject to substantial uncertainty in both the investment phase, which can be long and costly, as well as uncertainty about the market prospects of a commercialized product. Additionally managers possess operational flexibility allowing them to abandon projects that either become too costly to complete or whose market prospects turn out to be worse than the initial forecast. Real options analysis provides the techniques necessary to solve such complicated valuation problems.

So I thought that I would post a real options model demonstrating how to value a pharmaceutical R&D project. The paper that this post is based on is Schwartz (2004), Patents and R&D as Real Options, a free PDF of the working paper version is here. I’ll leave it to the paper to do most of the heavily lifting in terms of discussing the mathematics, and I’ll just give an overview of the model below.

This is the third post on real options analysis. In two previous posts I provided examples for valuing a natural resource investment and a real estate development. These earlier posts each solved the real option model using a different technique, Least Squares Monte Carlo simulation and binomial trees, respectively. The patent valuation model here also uses the Least Squares Monte Carlo (LSM) simulation technique to solve the model and value the patent. This technique is common to evaluate American and Bermudan style options where option exercise can occur prior to expiration. In the patent example, the manager has an abandonment option that can be exercised at multiple points prior to the expiration of the patent, thus we are working with an American style option.

Additionally the earlier real options posts only considered an environment where a decision maker faced a single source of uncertainty, the price of copper in the natural resource model and the market value of a completed apartment building in the real estate model. Reality is never so simple and usually a decision maker must confront multiple sources of uncertainty at once. The pharmaceutical valuation model here demonstrates how to handle two sources of uncertainty. It is straightforward to extend the model to account for other sources of uncertainty if need, such as stochastic interest rates.

As in the previous posts I constructed this model in Analytica. You can view and alter the model with the free version.

Eventually I will post a version of these models in the open source programming language Julia or maybe even Go (which I am using more and more for data science, see this cool book, if you never thought of Go as a data science language).

Update 6/9/21: I have recreated this model in Go. Here is the GitHub link if interested. The Go version relies heavily on the Gonum libraries for scientific and numerical programming.

Let’s jump in.

The Model

The setting for this model is the valuation of a pharmaceutical patent. The patent has a legally defined lifetime before it expires, which is 20 years in the United States. The patent’s lifetime is divided into an investment phase where research and development is carried out to create and test the drug, and a sales phase where the drug is commercialized and sold to consumers. Upon patent expiration the company loses the ability to charge monopoly prices and will instead receive a competitive price for the drug.

During the investment and R&D phase new information is revealed about both the the possible annual cash flows for a commercialized drug and the expected total cost to completion for the R&D. Both of these quantities are subject to substantial uncertainty and these uncertainties are key components to valuing the patent. The information uncovered during investment provides managers with the flexibility to abandon losing projects during the investment phase and avoid large loses from bringing a substandard product to market. This abandonment option adds significant value to the project as the model below will demonstrate.

Now let’s turn to the user panels to get a feel for the inputs of the model. Balloon help is enabled so if any of the input items are not clear, hover your mouse over the name and a description will appear:

Investment Cost assumptions

The first set of input assumptions is for the investment process. These inputs determine the possible evolution of the cost to completion at each decision point in the model. A decision point is when a manager can choose either to commit further investment to the R&D or abandon the project. In this model the decision points are at the start of each quarter during the year. Note that the cost volatility input captures the uncertainty for the cost to completion. This value can be estimated from data on similar projects.

The chance of failure input deserves special explanation as it is not part of the cost simulation that you see below. Chance of failure is the probability that the value of the project drops to zero immediately. Events in this category include a rival bringing a similar product to market first or the drug being discovered to be unsafe. Since these events are modeled as a Poisson process independent of each other and uncorrelated with the market, they don’t have to be simulated explicitly. These events are accounted for through an increase in the discount rate used to assess project value during the investment period.

Below are five possible simulation results for the cost to completion from the 30,000 different simulation runs that the model executes.

In the first period the cost to completion is close to the $100MM estimated cost and then decreases in an uncertain fashion over time as quarterly investments are made. Note that two of the runs are well above the average expected time to completion of 40 quarters. It is investments like these that are prime candidates for abandonment, as it becomes increasingly unlikely that the company will be able to recoup their expenditures and earn a profit.

Just a final comment on the investment process: while traditionally pharmaceutical R&D is broken into three distinct phases, for simplicity, in this model there is only one investment phase. Additional phases are straightforward to add, see section 4 of Schwartz’s paper for a discussion and this paper for a similar model involving a three phase pharmaceutical R&D program. For more on modeling investment cost uncertainty see Pindyck (1993), Investments of Uncertain Costs (PDF).

Product Market Assumptions

The next set of assumptions in the user panel is for the net sales cash flow. The net sales cash flow is the cash flow received after marketing and production costs. This cash flow only accrues to the firm after a successful R&D process has been completed.

For this model the cash flow is modeled as a geometric Brownian motion process. There is a drift term which is the expected rate of annual change and a volatility term that captures the uncertainty over future cash flows. Below is a chart of five different possible simulations for the cash flow. Note that these cash flows are the “risk neutral” cash flows, which are the risk adjusted cash flows used for valuation purposes.

The model thus captures the potential variability of the net sales cash flow across different simulation runs. There is a general drift down because of the risk premium that needs to be accounted for with these cash flows.

Now a geometric Brownian motion model may not be ideal for pharmaceuticals. Typically pharmaceutical sales start low and then increase to a peak sales level that decreases sharply once the patent expires. This type of structure can be accommodated within the simulation framework by adding a deterministic life cycle component to the model. This is one advantage of Monte Carlo simulation over using binomial trees, the underlying simulation process is highly customizable to the problem at hand. See Chang (2011), Monte Carlo Simulation for the Pharmaceutical Industry, chapter 8, for a model of drug adoption and sales.

Valuation Assumptions

The last set of assumptions are for the valuation of the model. The model uses the CAPM to derive a risk premium for the cash flow process. The risk free rate is constant in this model but stochastic interest rates could be added easily as another source of uncertainty. The Pharma beta is just the stock market beta on relevant pharmaceutical stocks.

Solution Procedure

Before I discuss the results let’s briefly outline the solution procedure. It is called a least squares Monte Carlo algorithm because it combines regression analysis (least squares) with Monte Carlo simulation. It first simulates the uncertain variables using Monte Carlo simulation forward through time as the variables depend on quantities in the previous time period to simulate current period values. The algorithm then starts in the final time period and works its way backward using the following calculus. If the investment phase has ended then the project value in each quarter is the discounted value from the next quarter plus the net cash flow of the current quarter. No abandonment option can be exercised here since it is always better to receive positive net cash flows.

If the project is in the investment phase then a decision must be made. The decision is whether to abandon the project driving the value to zero or invest in another quarter of R&D. The decision rule uses regression analysis to estimate the value of the project in the current period based on the discounted project value from the next quarter and the net cash flow and cost to completion in the current quarter. If the estimated project value is greater than the quarterly investment amount then the investment is made, otherwise the project is abandoned.

This process is iterated until the first period of the model. These values are then discounted once more and averaged. This average is the estimate of the real option value of the patent. Note that the algorithm I used is slightly different than discussed in the paper. The algorithm here is adapted from the LSM algorithm discussed in Glasserman (2004) chapter 8.

The Results

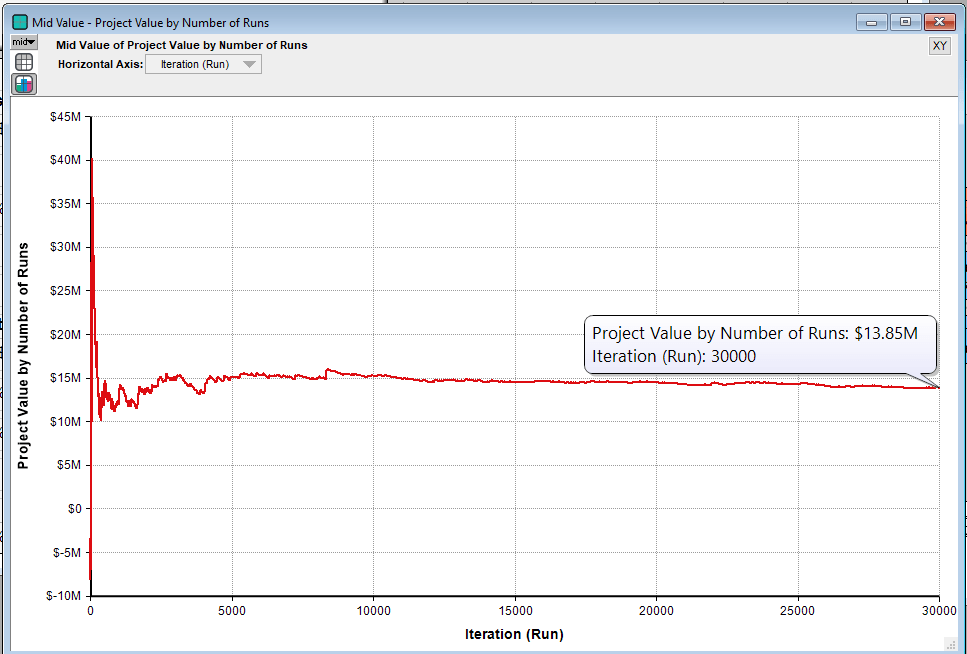

In the paper, Schwartz calculates the static NPV of this pharmaceutical project to be -$7.4MM. However the model’s estimate of the project’s value is $13.85MM. In this case the option accounts for about $21MM in value. Schwartz estimates the project value to be between $13-14MM, which is in line with the model here. As we see, the ability to abandon a losing project early creates a tremendous amount of value.

Note that Monte Carlo simulation will only provide an estimate of the project’s value and this estimate is dependent on the number of runs in the simulation. So below is a chart of the project’s value as the number of simulation runs increases, which clearly indicates that the value is settling down as the number of runs increases to the range estimated by Schwartz.

In the paper, Schwartz discusses a number of extensions and sensitivity analyses that I leave for you to explore. If you have any questions or comments please feel free to email me!

Pingback: Valuing Swing Options with Monte Carlo Simulation | Freehold Finance